In case anyone wondered why we ended the past 4 Journals with the ‘relative’ ECB meeting, the answer was clear as the 8:30 Trichet conference began!. Chart of ES is below of the move commencing on the dot……

Just as we concluded our frustration sound-off last night wondering what a "relative" catalyst for this market is. We had an answer. By the opening bell, we had as many as 3 with a change of heart saying risk should come back and these will matter ("relative"). …Here they are again…

Risk should come back...these catalysts should matter

*China export includes a whopping US#

*China Pension...$114 billion National Social Security Fund, said euro will be able to weather the sovereign debt crisis; "I do believe the euro will gradually stabilize and survive the crisis."

*Trichet every word pushing euro higher/ SPX, calming mkts

Firstly, we`ve been discussing the 'fumbling' of Trichet recently as a cause for much of the heartache recently. We concentrated on the ECB this week because in the back of our minds, he couldn't fumble again as he must have had some PR training by now or more like big money guidance this time around...."ECB later this week… Something will give here in Europe this week and will be a positive catalyst for the markets or else"….. Just like Geithner had you may recall when he started at the helm. It wasn`t the fact some wild solution, intervention of sorts would come, all he needed was touch on all the points (as he did) to de-stress the market and give it some calmness.

Secondly, Even though the China export# was leaked yesterday, it’s relevance all of a sudden became a catalyst and all the talk. One thing not being mentioned about the number, including the fact it beat consensus by something like 16% was that US shipments rose 23.5% m/m and even Europe rose 19%m/m. Importantly, these are May numbers when supposedly the world was falling apart. Clearly, it was not and China growth is not accelerating downward as feared. Importance is this relieves an "overhang" on the market sickening it for 2-4 weeks.

Since the opening bell and right into the close, the talking head guests were adamantly disputing this move. Yes, recent volatility has the seasoned traders flustered, but the fact is they missed this move through many technical resistance areas. It's probably unfathomable that we even closed at SPX 1087 for today's naysayers.

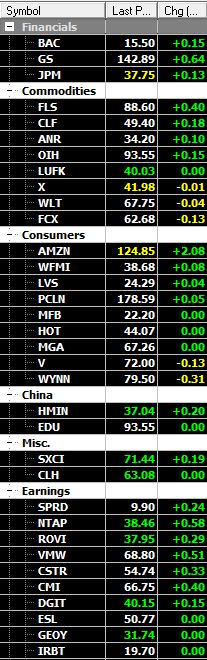

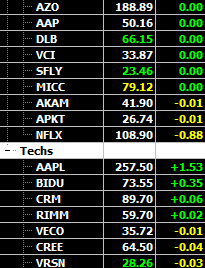

As we said this week, .." To gain some control back for the Bulls, we need to get over “R” at 1071 and than 1076." Well, we did this and beyond on a closing basis!. So, besides being technically relevant, we think 2 major overhangs got a lift today (Europe/ China). Not lifted completely, but a lift and that's a start for investors to begin starting to get off the sidelines. Good thing is still today's move was largely ETF based, individual stocks have catching up to do. Many are still you can say trading at 1040 levels. This day and the catalysts involved will only last so long, but we definitely think it will get investors thinking as risk is to the upside with many not positioned for it into June Q end!.

All in all, today was a Goal for the Bulls and we can enjoy some World Cup footy action in some peace!.

Demi/ YourPersonalTrader

Demi/ YourPersonalTrader