Oh, those shorts, who tried to press the issue of a Bull ‘blown oppy’ yesterday were rudely (once again) beaten by the ‘resiliency’ of this market as it bounced fast off the opening bell SPX 1178 touch(off ~20 points since Monday’s fresh high).

They were broken by using the old adage of a stronger USD/weaker Euro = lower equity prices, ignoring what was pointed out recently here that rotation from TSY’s was going to happen as QE2 expectations gets priced in. (see DJIM #42...“..but still equities did not sell off on the higher USD, This could be because rotation/liquidity into stocks from Treasuries is the natural course…and market remains steady because individual groups get enough liquidity to sustain it. ). This was overwhelming theme today as 10yr TSY’s made a big move crossing a trendline at 2.65% from April, while USD got a bid, but the market ‘surprisingly’ to the Bears did not drop. This is quite positive to hold up as we did.

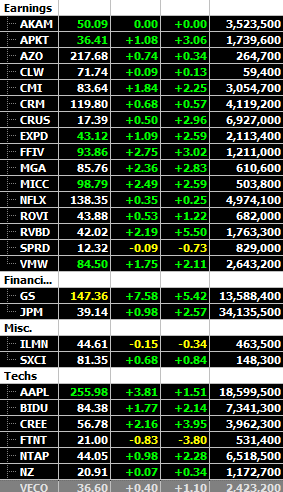

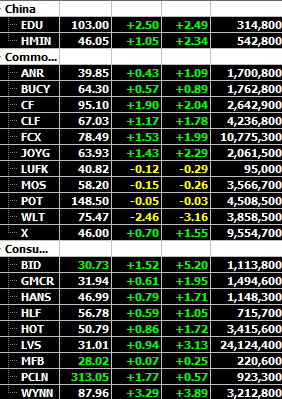

As noted, fixate on individual stocks and not the stalling market for oppy’s to trade. So, while the SPX traded in a very narrow band after 10am, our DJIM listed stocks, including some bolded yesterday added strong follow through. Notably, RIMM powered to a 10% intraday H, our little MOTR, motored another 15% before running out of the 9ema play, right back down the hill. BID >3% and MCP to a NCH. BIDU, NFLX, post -EPS were making fresh NCH‘s. The clouds-virts were strong with RVBD, FTNT extending post earnings gains as well. The group was also helped by CML retaining advisors for a possible sale (v.nice earnings AMC was a no brainer, if you announce such a deal possibly in the making hours before). AMC, FFIV,EQIX helped out the group some more. The premise here that there is room to run after a gap off earnings was shown again today in MIPS ( it’s another stock that has been mentioned in M&A discussions). Also, note if the market gets into any defensive rotation soon LIFE, ILMN are two strong earnings today to go to, probably even right away tomorrow.

Clearly, if you want to outperform now, it’s primarily selective earnings stocks we should be driving as broad market’s uncertainty is abound around next week’s catalysts .

Demi/ YourPersonalTrader

Demi/ YourPersonalTrader