It’s been nearly two weeks since noted..”Earnings, if they keep at this pace 'will trump' any Eco data-FOMC statements..”..

Immediately, following this statement we ran into a few days of roadblocks where earnings were missing the revenue top line and most proclaimed Macro victorious over Micro (corporate) as the SPX dropped to 1055. Now 5 trading days later, yes only 5, the SP hovers near 1115, some 60 handles higher on the heels of Micro winning out. Of course, this stands till August …“….because eco`data will be sparse until August hits and we see how July was. Starting next week, we will live by the guidance from the CEO/CFO`s." In other words we have some time to climb higher if we get through a boatload of technical ‘R” numbers around today’s close, but once August hits it will be eyes on US eco data’ starting with ISM’s to verify what the corporations and global markets are saying.

The good part is we have good things on the Bulls back coming into August data...Micro (earning) fundamentals, Western Europe accelerating into 2H and China ‘bottoming’, plus FINREG/ Stress tests over with. We didn’t have any of this when the market was toying with a potential summer under 1K SPX in June.

Today, market had FDX add some validility to the global picture, but we’ve had this already here at DJIM 2 weeks ago as part of an improving global snapshot.. “EXPD , bot some, 30% upside is a great pre-announcement, should help FDX -transports”.

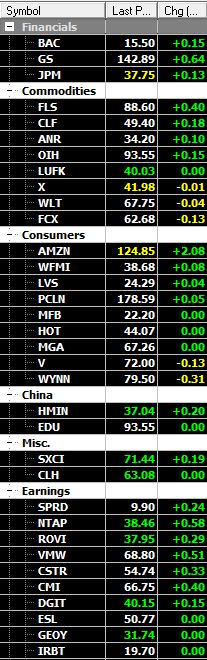

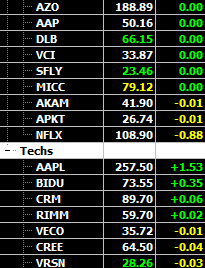

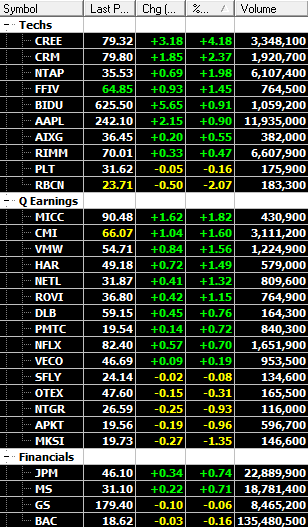

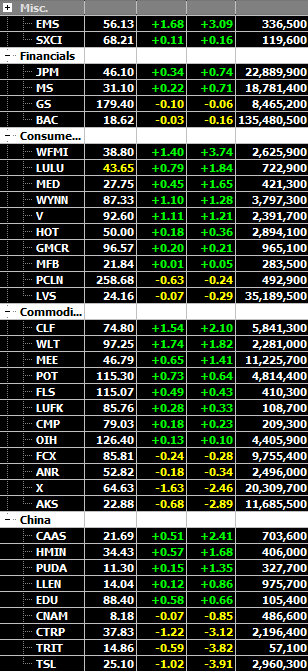

A few other earning highlights noted VMW , CRUS, also making NCH (New highs). Past DJIM Q's/2010 plays, AZO, RBCN, OVTI, NTAP, ROVI, CRM continue to grind away at new highs. We also have APKT, DLB on 5-6 trading day moves that we suggested as potential run ups into their earnings this Thursday flirting at NCH‘s..“Look at tech reporting soon on sell off..APKT DLB etc.on this 20 day hit. Apr 16. Also AMC, VECO report shows DJIM LED stocks (CREE AIXG RBCN ) still have momentum in ‘10.

In conclusion, if the breadth of the market stays on par and/or performance chasers come, a try at the 50% retrace would be in the cards. This is also where we have June peak to contend with. Still, don’t think these levels should cloud our thinking with new earning plays emerging and getting some recent ones back on pullbacks remaining the premise. Starting tomorrow, looking for a close over June high close of 1118 for ~1130 sooner than later, otherwise a dip is probably in order.

Demi/ YourPersonalTrader

Demi/ YourPersonalTrader